Choosing the Right Business Structure in the USA

Starting a business is an exciting journey, but before you launch your dream, there is one big decision you’ll need to make: what type of business structure is right for you?

Your business structure is not just a box to check, it affects everything from how much tax you’ll pay, to how much paperwork you’ll deal with, to whom your personal assets are protected if something goes wrong. It also impacts your ability to raise money, attract investors, and grow your business over time.

This isn’t a decision you want to rush. Choosing the wrong setup can lead to unnecessary costs, legal headache, or even limit how far your business can grow. But don’t worry, we are here to make it simple.

In this article, part of our series on starting a Business in the USA, we’ll walk you through the main types of business structures. Just simple, useful and practical information to help you make the right choice from day one.

Sole Proprietorship

A Sole Proprietorship is the most basic type of business structure in the US and it is incredibly easy to start. In fact, if you’re running a business on your own and have not registered as an LLC or Corporation, you are probably already a sole proprietor without even realizing it.

This structure gives you full control over your business. However, it does not create a separate legal entity, which means there is no legal distinction between you and your business. If your business has debts or faces a lawsuit, your personal assets could be at risk.

Sole Proprietorships are ideal for low-risk businesses, freelancers or first-time entrepreneurs who want to test their idea before committing to a more formal business structure like an LLC or Corporation.

Advantages

- Easy and Inexpensive to set up – There is no need to file with the state (unless you are using a trade name)

- Complete control – You make all decision and keep all profits.

- Simplified taxes- Business income is reported on your personal tax return (Form 1040 + schedule C), avoiding separate business tax filings.

- Fewer regulations- No Corporate formalities like board meetings or annual reports.

Dis-advantages

- Unlimited Personal Liability- Since there is no legal separation between you and your business, you are personally responsible for any debts, lawsuits or obligations.

- Harder to raise capital- You can’t sell shares, and many banks are hesitant to lend to sole proprietors.

- No continuity- The business legally ends if the owner dies or becomes incapacitated.

- Limited Growth potentials- Investors and partners usually prefer more formal structures.

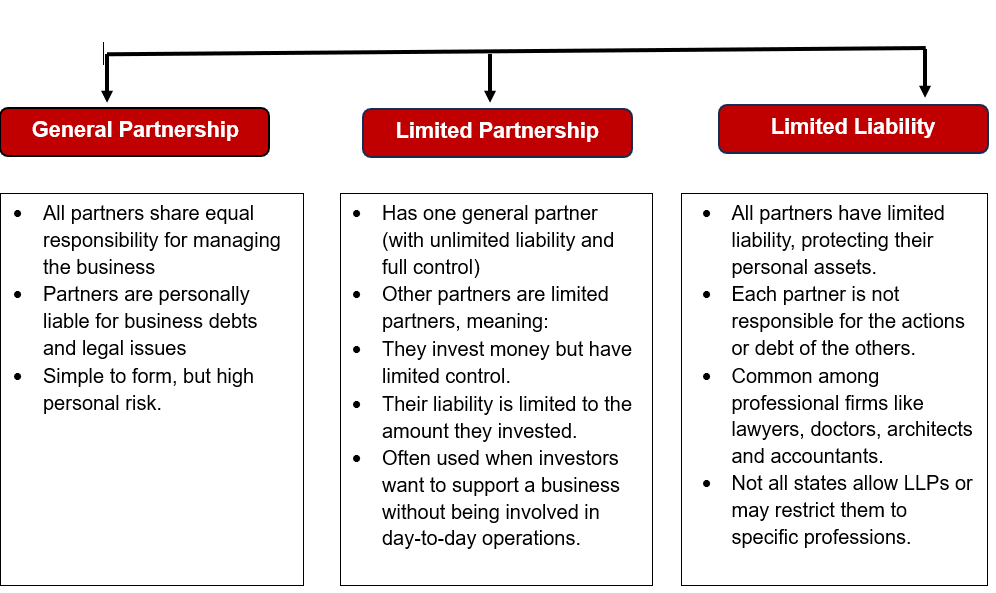

Partnership

A Partnership is one of the easiest ways for two or more people to start a business together. Like sole proprietorship, it is relatively simple to set up, but instead of one owner, a partnership involves two or more co-owners who share in the business’s profits, losses and responsibilities.

Key features of a Partnership

- Business is owned by two or more people

- Each partner contributes money, skills or time

- Profit and losses are usually shared based on the agreement

- Business income is passed through to each partner’s personal tax return

- Requires a partnership agreement (highly recommended)

Types of Partnerships

Advantages

- Easy and affordable to start

- Shared responsibility- work, risks and costs are split.

- More capital – more owners can mean more money to invest

- Tax benefits – profits pass through to partners’ personal tax returns (no corporate tax)

Dis-advantages

- Personal Liability – especially in general partnership, you are responsible for business debts.

- Shared decision making – disagreements can affect business operations

- Profits must be shares – even if one partner contributes more, make more efforts

- No separate legal identity (Unless it is an LLP)

Limited Liability Company (LLC)

It is one of the most popular business structures in the US. It offers a unique combination of personal liability protection, tax flexibility and ease of management, making it a top choice for both new and growing businesses.

Think of an LLC as the best of both worlds: it gives you the legal protections of a corporation while offering the simplicity and tax benefits of a sole proprietorship or partnership.

Advantages of an LLC

- Personal Asset protection - This is the #1 reason many entrepreneurs choose an LLC. If your business is sued or can’t pay its debts, your personal assets like your house, car and savings are generally protected. The liability is limited to what the business owns- not what you own personally.

- Pass- through Taxation - Unlike corporations that pay taxes twice (once on the business and again on shareholder dividends), LLC profits and losses pass through to your personal tax returns. This often results in lower overall taxes.

- Flexible management- LLCs are not required to have directors or officers. You can run the business yourself (single- member LLC) or with partners (multi-member LLC). You also decide how profits are shared and how decisions are made.

- Easy to form and Maintain - Forming an LLC involves filing basic paperwork (usually Articles of Organization) with your state and paying a fee. Ongoing requirements are minimal- no annual board meetings, complex records or shareholders rules like with corporations.

Things to be aware of

- Self-employment Taxes- Members of an LLC are considered self-employed, meaning you shall need to pay self-employment taxes (for social security and Medicare) on your share of the profits. However, you can elect corporate taxation to potentially reduce this burden

- State rules may vary- Some states require LLCs to be dissolved and re-formed if a member leaves or joins- unless your Operating Agreement says otherwise. It is important to create a strong Operating agreement from start to avoid this issue.

Who should consider an LLC?

An LLC is a smart choice if you:

- Want to protect your personal assets

- Are running a medium to high risk business

- Have (or plan to have) partners or investors

- Want a flexible structure that grows with your business

Corporation

A Corporation is a separate legal entity created by filing with the state. Unlike a Sole proprietorship, partnership, or even an LLC, a corporation has a life of its own- it exists independently of its owners (shareholders) and can own property, enter contracts, sue or be sued and continue to operate even if ownership changes.

There are 2 main types of corporations in the US: C Corporations (C-Corps) and S Corporations (S-Corps).

C Corporations (C-Corps)

It is the default form of corporation in the US. It is completely separate legal and tax entity from its owners, which means the corporation itself is responsible for paying taxes, debts and legal obligations- not the individuals who own it.

Advantages

- Strongest Personal Liability Protection – shareholders are generally not personally responsible for business debts or lawsuits. Your personal assets are safe, even if company is sued or goes bankrupt.

- Unlimited Growth Potential – C-Corps can issue multiple classes of stock and have unlimited shareholders, which makes it easier to raise capital

- Separate Legal Existence – A C-Corp continues to exist even if a shareholder leaves, sells shares or passes away. This makes ownership transfer smooth and long-term planning easier.

Dis-advantages

- Double taxation – first, the corporation pays taxes in its profits. Then, if it distributes profits to shareholders as dividends, those are taxes again on the individual’s tax return.

- More complex and costly to set up –

- Must File Article of incorporation

- Need bylaws, annual meetings and a board of directors

- More paperwork and strict compliance rules

- Ongoing reporting and Record keeping requirements

- Maintain formal minutes, resolutions and detailed corporate records.

It is not a different type of corporation- it is a tax status that a corporation can elect by filling Form 2553 with the IRS.

The S- Corp status allows the business to avoid double taxation by passing profits and some losses directly to shareholder’s personal tax returns. The corporation does not pay federal income tax itself (with a few exceptions).

When to Choose an S-Corp

An S-Corp could be right for you if:

- You’re eligible for S-Corp status and want to avoid double taxation

- You want to save on self-employment taxes

- You’re running a small to mid-sized business with limited shareholders

- You still want liability protection and structure, but with tax efficiency

Advantages

- Avoids Double Taxation- Unlike a C-Corp, an S-Corp’s profits are only taxes once, on the shareholder’s personal tax returns.

- Liability Protection- Like any corporation, an S-Corp offers limited Liability, protecting owners from personal responsibility for business debts or lawsuits.

- Ongoing Business life- S-Corps continue operating regardless of changes in ownership, offering stability and continuity.

- Saving on Self- Employment tax- Shareholders who also work for the company can be paid a salary (which is taxed), and remaining profits can be distributed as dividends, which may not be subject to self-employment tax potentially lowering the overall tax burden.

Dis-advantages

Strict Eligibility Requirements

- Must be a U.S.-based business

- Limited to 100 shareholders

- Shareholders must be U.S. citizens or residents

- Can issue only one class of stock

- Cannot be owned by corporations or partnerships

IRS Approval Required

- Must file Form 2553 to elect S-Corp status

- Missing deadlines can delay or block your S-Corp status

Same Formalities as a C-Corp

- Must still hold annual meetings, keep records, and file detailed reports

- Must pay reasonable compensation to shareholders who work in the business, or risk IRS penalties

State-Level Differences

- Some states don’t recognize S-Corp status and will tax your business like a C-Corp

- Others may impose additional state taxes or franchise fees

Frequently Asked Questions (FAQ)

What is the most common or 'best' business structure for a new small business in the USA?

The Limited Liability Company (LLC) is often considered the most popular and "best starting point" for new small businesses. It offers the crucial benefit of personal asset protection (shielding your home and savings from business debt/lawsuits) while retaining the simplicity and tax flexibility (pass-through taxation) of a Sole Proprietorship.

If I start as a Sole Proprietor, can I change to an LLC later?

Yes, absolutely. Many entrepreneurs start as Sole Proprietors because it is the easiest and cheapest option. However, as the business grows, takes on more risk, or starts making significant revenue, it is highly recommended to convert to an LLC or Corporation to gain liability protection.

What is the main difference between an LLC and an S Corporation (S-Corp)?

An LLC is a legal structure, primarily chosen for liability protection and management flexibility. An S-Corp is a tax election (a tax status, not a separate legal entity) that an LLC or Corporation can choose to help the owner potentially save money on self-employment taxes. The main difference is the purpose: one protects assets, the other optimizes taxes.

What is 'double taxation' and how does an S-Corp election help avoid it?

Double taxation is a risk primarily faced by C Corporations. It occurs because the corporation pays income tax on its profits, and then the shareholders pay income tax again on the dividends they receive from those profits. An S-Corp election allows the business's profits and losses to "pass through" directly to the owner's personal tax return, avoiding the corporate income tax layer entirely.

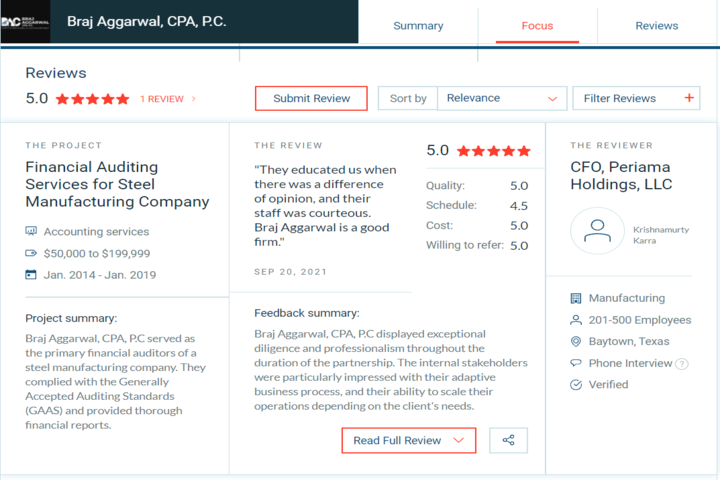

Why is consulting with a CPA, like Braj Aggarwal, CPA, P.C., essential when choosing a structure?

Consulting a CPA is critical because the decision is driven heavily by tax implications and future growth strategy. A CPA, such as Braj Aggarwal, CPA, P.C. in New York, can analyze your projected revenue, your business goals, and the laws in your specific state to recommend the most tax-efficient structure (e.g., whether to elect S-Corp status) and ensure you comply with all federal and state filing requirements from day one.

Don't leave your financial future to chance. Choosing the right business structure is the most critical decision you'll make, impacting your taxes, liability, and growth trajectory for years to come. While this article provides a great foundation, every business has unique needs. For personalized advice tailored to your specific goals and projections, consult with the experts. Contact the dedicated team at Braj Aggarwal, CPA, P.C., your trusted CPA Firm in New York, to ensure you Start Smart and set up your US business for maximum success and tax efficiency from Day One.